Global remote hiring in Architecture, Engineering, and Construction is accelerating, and the tax exposure that comes with it is outpacing most firms’ compliance awareness. McKinsey reports the construction industry has “difficulties in attracting digital talent,” which slows down innovation, and expects remote-working practices to be a lasting change factor. But hiring a BIM coordinator from India, a CAD drafter from Eastern Europe, or a remote architect from Latin America triggers tax obligations that most AEC firms are not prepared for, withholding requirements, permanent establishment risk, IRS form collection, and VAT or GST invoicing rules. This article covers every layer, clearly and practically.

This article provides general information only and does not constitute legal or tax advice. Consult a qualified tax professional before making international hiring decisions.

Why Global Hiring Is Rising in the AEC Industry

The construction talent shortage is pushing AEC firms to look beyond their local markets, and the economics make a compelling case for doing so.

AGC reported 85% of firms have openings, and 88% of those firms are having trouble filling at least some positions. For architecture and engineering firms, the picture is similar: demand for BIM coordinators, CAD drafters, and design documentation specialists routinely outpaces local supply in major U.S. markets.

Three forces are driving global AEC hiring:

- Cost advantages over local hiring: A BIM specialist with five years of Autodesk Revit and BIM 360 experience costs $65,000–$90,000 annually as a U.S. full-time employee. An equivalent remote contractor based in Eastern Europe or South Asia typically invoices $15,000–$35,000 per year for the same technical output on the same design documentation deliverables.

- Access to specialized talent across regions: Remote contractors bring discipline-specific expertise, BIM coordination, CAD production, and construction administration support that is genuinely scarce in many U.S. metro markets. Geography no longer limits who your AEC firm can work with.

- Production capacity without headcount permanence: International independent contractors scale with your project pipeline. A firm managing a peak design phase can add a remote CAD drafter or BIM coordinator for six months without committing to a permanent hire.

What Changes When You Hire an AEC Contractor in Another Country?

Hiring a local freelancer and hiring an international independent contractor are not the same transaction, even if the invoice looks identical and the deliverables are the same CAD drawings or BIM files.

Why This Is Not the Same as Hiring a Local Freelancer

A local freelancer operates within one tax jurisdiction. You pay them. They handle their own taxes. You issue a Form 1099-NEC if they are a U.S. person who earned over $600. That is the full extent of your tax obligation in most cases.

An international contractor introduces multiple overlapping tax jurisdictions simultaneously. Your firm’s payment crosses a border. The contractor’s home country has its own tax rules. The IRS has specific requirements for payments to nonresident aliens. Tax treaties between countries may or may not apply. Permanent establishment risk may exist depending on what the contractor does and where. VAT or GST may appear on their invoice depending on their jurisdiction.

Every one of these layers requires a deliberate compliance decision, not a default assumption carried over from your domestic contractor process.

The Tax Questions AEC Firms Need Answered Before the First Invoice

Before a single payment leaves your account, your AEC firm needs answers to these questions:

- Is this person legally classifiable as an independent contractor, or does the nature of the AEC work relationship create employee classification risk?

- Where are the services being performed, inside or outside the United States?

- Is the payment subject to U.S. withholding tax, and if so, at what rate?

- Does a tax treaty between the U.S. and the contractor’s country affect the withholding rate?

- What IRS forms does your firm need to collect, Form W-8BEN for individuals or Form W-8BEN-E for entities?

- Does the contractor’s invoice include VAT or GST, and how does your firm account for that?

- Could the contractor’s work pattern or job site presence create permanent establishment risk in their country?

None of these questions has a universal answer. Each depends on the contractor’s country of residence, the nature of the AEC work, where the services are physically performed, and the specific tax treaty, if any, between the U.S. and that country.

Start Here: Are They Really a Contractor?

Before any tax form, withholding calculation, or permanent establishment analysis, the first question your AEC firm must answer is the most fundamental one: Is this person actually an independent contractor?

Getting this wrong is expensive. Misclassifying an employee as an independent contractor exposes your firm to back taxes, penalties, and interest in both the U.S. and the contractor’s home country simultaneously.

Contractor vs Employee: The Classification Test That Comes First

The IRS applies a behavioral, financial, and type-of-relationship test to determine whether a worker is an employee or an independent contractor.

The three-factor framework:

- Behavioral control: Does your firm control how the work is done, not just the outcome? Daily direction, set working hours, and mandatory tools all point toward employee classification.

- Financial control: Does the contractor work exclusively for your firm? Do they invoice multiple clients? Do they provide their own software and equipment? Exclusivity and firm-issued tools both signal employment.

- Type of relationship: Is there a written contractor agreement? Are there employee-style benefits, paid leave, health coverage, and structured performance reviews? Long-term, open-ended engagements with no defined project end date significantly increase employee classification risk.

Foreign tax authorities, including HMRC in the UK under the IR35 framework and equivalent bodies across the EU and Asia-Pacific, apply similar tests. A worker who passes the IRS contractor test may still be classified as an employee under their home country’s rules. Both determinations matter when cross-border payments are involved.

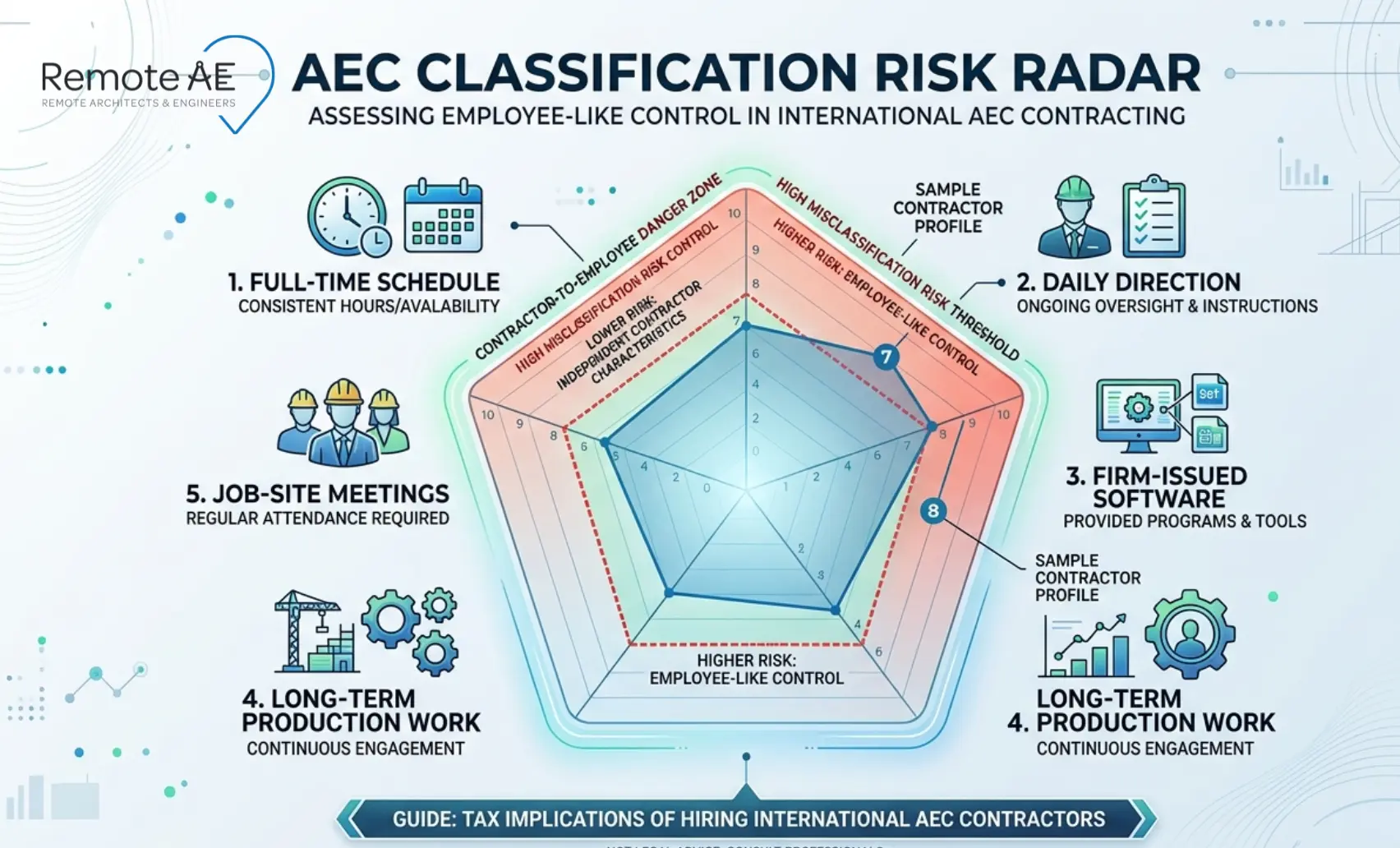

Why AEC Work Blurs the Line Faster Than Other Industries

Architecture, Engineering, and Construction work patterns create classification risk that does not exist in most other remote contractor relationships. Here’s why:

- Full-time schedules: A remote BIM coordinator working 40 hours per week on a single AEC firm’s projects, producing design documentation, attending daily coordination calls, and managing a BIM 360 model looks operationally indistinguishable from a full-time employee.

- Daily direction from project managers: When a project manager assigns tasks, reviews work, and provides real-time feedback to a remote CAD drafter every working day, that level of behavioral control pushes the relationship toward employment classification.

- Firm-issued software access: Providing a contractor with licensed access to Autodesk Revit, Autodesk Construction Cloud, or Procore under your firm’s account signals financial control, a key employment indicator in the IRS framework.

- Long-term production work: An international contractor engaged continuously for 18 months on ongoing design documentation and BIM coordination work with no defined project end carries substantially higher classification risk than a contractor hired for a discrete, deliverable-based scope.

- Job site meetings or field coordination: A remote contractor who travels to U.S. job sites for field coordination, attends owner-architect-contractor meetings, or signs documents on your firm’s behalf introduces both employee classification risk and permanent establishment exposure simultaneously.

The fix before you hire: Structure the engagement around deliverables, specific CAD drawings, BIM model milestones, and design documentation packages, not around time-based availability.

Use a written independent contractor agreement that defines scope, payment terms, and the absence of employment benefits. Have a qualified employment attorney review the agreement before the first invoice.

Core Tax Considerations When Hiring International Contractors

Once you have confirmed legitimate independent contractor classification, three core tax issues govern every international AEC contractor engagement. Each one requires a specific compliance decision before payment begins.

Withholding Tax Requirements

The U.S. generally requires businesses to withhold 30% of payments made to nonresident aliens for U.S.-source income. That withholding rate can be reduced, sometimes to zero, by an applicable tax treaty between the U.S. and the contractor’s country of residence.

When withholding applies:

- The contractor is a nonresident alien for U.S. tax purposes

- The payment is for U.S.-source income, services performed inside the United States

- No valid tax treaty exemption applies to the payment type

When withholding typically does not apply:

- Services are performed entirely outside the United States, a BIM coordinator in India producing design documentation from their home office, never entering the U.S., generally earns non-U.S.-source income not subject to U.S. withholding

- A valid Form W-8BEN or Form W-8BEN-E is on file claiming a treaty-reduced rate, and the claim is valid under the applicable treaty

Permanent Establishment Risk

Permanent establishment, PE, is the tax concept that determines whether your AEC firm has created a taxable presence in a foreign country. If PE is triggered, the foreign country can tax your firm’s profits attributable to that presence.

What PE means in simple terms: Your firm has a permanent establishment in a country when it has a fixed place of business there, or when someone in that country has the authority to conclude contracts on your firm’s behalf.

How hiring abroad can trigger PE for AEC firms:

- A remote contractor who works exclusively and continuously for your firm from a dedicated office in their country may constitute a fixed place of business

- A contractor who negotiates contracts, signs agreements, or makes binding project commitments on your firm’s behalf in their country almost certainly creates dependent-agent PE

- A contractor who regularly attends project meetings in their country as your firm’s representative, even without formal signing authority, can attract PE scrutiny from local tax authorities

Risk factors specific to AEC firms:

- International contractors attending local authority meetings or planning consultations on your firm’s behalf

- Contractors signing off on local regulatory submissions using your firm’s name

- Long-term exclusive arrangements where the contractor operates as your firm’s de facto local office

- Contractors managing local subcontractors or vendors on your firm’s behalf in their jurisdiction

PE exposure is the highest-consequence tax risk in international AEC contractor hiring, and the one most firms discover too late.

Double Taxation Issues

Double taxation occurs when the same income is taxed in two countries simultaneously: the contractor’s home country taxes their earnings, and the client country applies withholding on the same payment.

How it affects both parties:

- Your AEC firm may be required to withhold tax on the gross payment, reducing what the contractor receives

- The contractor then pays income tax in their home country on the same earnings, potentially with limited credit for the withheld amount, depending on their jurisdiction

- Your firm may face foreign tax obligations in the contractor’s country if PE is triggered, meaning profits are taxed both in the U.S. and abroad

Why it matters in cross-border AEC projects: Tax treaties, bilateral agreements between countries that follow the OECD Model Tax Convention framework, exist specifically to prevent double taxation.

The U.S. has tax treaties with over 65 countries that reduce or eliminate withholding rates on certain payment types. Knowing whether a treaty applies, and claiming it correctly through Form W-8BEN, is the primary mechanism for avoiding double taxation on international AEC contractor payments.

Are VAT, GST, or Local Invoice Rules Part of the Deal?

Value-added tax and goods and services tax obligations vary significantly by contractor jurisdiction, and they frequently appear on invoices from overseas contractors without prior warning.

- EU-based contractors: May be registered for VAT and required to include it on invoices issued to non-EU clients, depending on the service type and jurisdiction

- UK contractors: Post-Brexit VAT rules apply. UK contractors providing services to U.S. firms generally do not charge UK VAT on exports, but confirm the specific service classification

- Australian and Canadian contractors: GST or HST may apply depending on the nature of the services and the contractor’s registration status

- Invoicing rules: Some jurisdictions require specific invoice content, tax registration numbers, service descriptions matching local tax classifications, and sequential invoice numbering. A contractor’s invoice that doesn’t meet local requirements can create compliance problems for their own tax filings, which can then affect your firm’s payment documentation

Confirm invoicing requirements in the contractor’s jurisdiction as part of the pre-engagement checklist, before their first invoice arrives formatted incorrectly.

U.S.-Based AEC Firms: The Rules That Usually Matter Most

For U.S. architecture, engineering, and construction firms hiring internationally, three IRS rules govern the majority of cross-border contractor payment scenarios.

When Form 1099-NEC Applies

Form 1099-NEC, used to report payments to independent contractors, applies to U.S. persons. It does not apply to payments made to foreign contractors for services performed outside the United States.

Specifically:

- If the contractor is a nonresident alien and has provided a valid Form W-8BEN or W-8BEN-E, you do not issue a Form 1099-NEC

- If the contractor is a nonresident alien but has not provided the required W-8 form, your firm may face backup withholding obligations

- If a foreign contractor performs any services inside the U.S., visiting a job site, attending a client meeting, or conducting field coordination, the U.S.-source portion of their payment may trigger 1099-NEC reporting requirements depending on their visa status and tax treaty position

The rule of thumb: Collect the W-8 form first. Once it is on file, the 1099-NEC question is resolved, you do not issue one, and you document the foreign status of the payment for IRS purposes.

When a Foreign Contractor Gives You Form W-8BEN or W-8BEN-E

Form W-8BEN and Form W-8BEN-E serve the same fundamental purpose. They certify that the contractor is a foreign person for U.S. tax purposes and establish the basis for any treaty-reduced withholding rate.

- Form W-8BEN is for foreign individuals, a nonresident alien architect, engineer, or construction specialist operating as a sole contractor

- Form W-8BEN-E is for foreign entities, an engineering firm, a BIM coordination company, or an architecture practice incorporated outside the U.S.

Key compliance points:

- W-8 forms are valid for three calendar years following the year of signing, track expiration dates, and collect updated forms before they lapse

- A contractor claiming a treaty benefit on the W-8BEN must provide their foreign tax identification number and identify the specific treaty article under which the benefit is claimed

- If the treaty reduces withholding to zero on service income, as many U.S. tax treaties do, your firm pays the full invoiced amount and retains the W-8BEN as documentation

Why Service Location Affects U.S. Source Income and Withholding

The IRS determines if income is U.S.-source based on where the services generating that income are performed, not where the contractor is based or where your firm is located.

This distinction has direct practical implications for AEC firms:

- A remote CAD drafter in Vietnam producing construction drawings from their home office earns non-U.S.-source income, generally not subject to U.S. withholding, regardless of treaty status

- The same drafter who travels to a U.S. job site for two weeks of field coordination earns U.S.-source income for the period of U.S. services, potentially subject to 30% withholding on that portion of their payment

- A remote BIM coordinator in Poland working within Autodesk Construction Cloud on a U.S. construction project, entirely from Poland, earns non-U.S.-source income for the remote portion of their work

A Simple Hiring Workflow for Staying on the Right Side of Tax Rules

Use this five-step process on every international AEC contractor engagement, before the first invoice, not after.

Step 1: Classify the Worker

Apply the IRS behavioral, financial, and type-of-relationship test before drafting any agreement. If the engagement structure creates classification risk, exclusive full-time schedule, daily direction, firm-issued software, open-ended duration, restructure it around deliverables before proceeding.

If classification is genuinely uncertain, obtain a qualified legal opinion. The cost of a one-hour consultation with an international employment attorney is far lower than the back-tax exposure from a misclassification finding.

Step 2: Confirm Where the Services Will Be Performed

Document the service location explicitly in the contractor agreement, in the scope of work, and in your internal payment records.

- Entirely outside the U.S., document this and confirm the non-U.S.-source income position

- Partially in the U.S., identify which activities will occur on U.S. soil, estimate the proportional payment value, and determine whether withholding applies to that portion

- Job site visits log every U.S. site visit date, duration, and purpose. These records protect your withholding decisions if the IRS questions the source income allocation

Step 3: Collect Forms and Invoice Details

Before the first payment:

- Signed contractor agreement in hand

- Deliverable-based scope of work confirmed

- Form W-8BEN or W-8BEN-E collected and verified

- Tax residency certificate obtained, where available

- Invoice format requirements confirmed for the contractor’s jurisdiction

- VAT or GST registration number documented if applicable

Nothing is paid until every item on this list is complete. No exceptions.

Step 4: Check Treaty, Withholding, and Local Registration Issues

- Confirm whether a U.S. tax treaty exists with the contractor’s country, and whether it reduces the withholding rate on service income

- Apply the correct withholding rate, 30% standard, treaty-reduced rate, or zero, where services are entirely non-U.S.-source

- Check whether the contractor’s jurisdiction imposes any local registration, withholding, or reporting obligation on foreign clients. Some countries require foreign firms paying local contractors to register with the local tax authority or withhold on their behalf

Step 5: Review PE and Site-Presence Exposure

Before the engagement begins, and again at the six-month mark for ongoing arrangements:

- Does the contractor have the authority to bind your firm contractually in their country?

- Is the contractor working exclusively for your firm from a fixed workspace?

- Has the contractor attended or will they attend regulatory or client meetings as your firm’s representative?

- Is the engagement structured with a defined end date?

- Does the contractor manage local vendors or subcontractors on your behalf?

Any confirmed item warrants a tax opinion on permanent establishment exposure before the engagement continues.

Common Mistakes AEC Firms Make With International Contractors

These four mistakes appear repeatedly across architecture, engineering, and construction firms navigating international contractor hiring for the first time.

Treating Every Overseas Hire Like a Standard Freelancer

- Applying the domestic freelancer process, signing an agreement, receiving invoices, paying in full, to an international contractor ignores withholding obligations, W-8 form requirements, and PE risk entirely

- The consequences surface later, IRS penalties for failure to collect W-8 forms, back-withholding assessments on payments to nonresident aliens, and foreign tax authority inquiries into PE exposure

Fix: Build a separate international contractor onboarding checklist that runs parallel to your domestic process. never substitute one for the other

Using the Wrong Tax Form

- Issuing a Form 1099-NEC to a foreign contractor who has provided a W-8BEN is incorrect, and signals to the IRS that your firm misclassified a foreign payment as a domestic one

- Collecting a W-8BEN from a foreign entity, which should receive a W-8BEN-E, creates a documentation gap that invalidates the treaty benefit claim

Fix: Train whoever manages contractor payments on the W-8BEN vs W-8BEN-E distinction before the first international invoice is processed

Ignoring Local Tax Advice Because the Contractor Is “Remote”

- Remote delivery does not eliminate local tax obligations. A BIM coordinator working from their home office in Germany is still subject to German tax law, and your firm’s engagement structure may have German tax implications your U.S. accountant is not aware of

- IR35 in the UK, for example, can reclassify a remote contractor as an employee for tax purposes if the engagement meets certain criteria, exposing both parties to back-tax liability regardless of what the contract says

Fix: Engage a local tax advisor in the contractor’s jurisdiction for any engagement expected to exceed six months or $30,000 in total value

Assuming Site Work or In-Country Meetings Change Nothing

- A remote CAD drafter who visits a U.S. job site for two weeks of construction documentation support has generated U.S.-source income for that period, even if 95% of their work is performed overseas

- A remote architect who attends a planning meeting with a local authority in their country as your firm’s representative has potentially triggered permanent establishment exposure, regardless of how the contractor agreement is worded

Fix: Flag every job site visit, in-country meeting, and client-facing activity in the contractor’s jurisdiction as a potential tax event. Document it. Review it against your PE checklist. Consult your tax advisor if the activity involves contract authority or regulatory representation.

When It Makes Sense to Use a Managed Remote Hiring Partner

International contractor tax compliance is manageable, but it is not simple. At a certain scale of remote hiring, the compliance burden of DIY cross-border contractor management outweighs the cost of working with a managed hiring partner who has already solved these problems.

Signs Your Firm Has Outgrown DIY Cross-Border Contractor Hiring

- You are managing three or more international contractors simultaneously across different jurisdictions, each with different withholding rates, treaty positions, and invoicing requirements

- A contractor’s W-8BEN has expired, and no one on your team noticed until an IRS inquiry arrived

- Your finance team is spending more time on contractor tax documentation than on project financial management

- A contractor recently visited a U.S. job site, and no one assessed the U.S.-source income implications before the payment was processed

- You have received an invoice with VAT included from a European contractor, and no one on your team knows whether to pay it, reject it, or account for it separately

- Your firm is expanding into new markets, Latin America, Eastern Europe, Southeast Asia, where local tax rules are unfamiliar, and treaty positions are untested

Any two of these signals indicate that a structured managed hiring approach will deliver better compliance outcomes and lower administrative costs than continuing to manage international contractor hiring internally.

How Remote AE Helps Reduce Hiring Friction for AEC Teams

Remote AE has been delivering pre-vetted virtual assistants tailored specifically for the Architecture, Engineering, and Construction industry for more than 15 years.

Every assistant brings a minimum of five years of AEC-specific experience, in BIM coordination, CAD production, design documentation, construction administration, and project coordination, across the tools your projects run on.

Here is what that means for your firm’s international hiring process:

- Industry-specific expertise: Remote AE assistants arrive fluent in AEC workflows, Autodesk Revit, BIM 360, Autodesk Construction Cloud, CAD production, and design documentation standards. No tool training. No workflow orientation. Production from week one.

- Guaranteed quality and reliability: Deliverables meet your defined QA/QC standards, or the issue gets resolved immediately, not at the next review cycle

- No long-term commitment: Engage on a project basis or as an ongoing resource. The model adapts to your pipeline, not the other way around

- Staffing from $499/week: Professional virtual AEC assistant support accessible for firms at every growth stage

- 52% of first-time clients hire a second remote assistant within their first year, a direct reflection of the output quality and workflow integration Remote AE delivers from day one

- No upfront costs: Consult with the Remote AE team without any initial financial burden. There is no cost or obligation until the contractual phase begins. Evaluate fit before you commit

- Risk-free replacement: In the first year, Remote AE offers risk-free replacements for up to two virtual assistants. If a placement does not meet your standards, it gets resolved without disrupting your active project or your budget

Hire International AEC Talent Without the Compliance Headache!

The tax implications of hiring international AEC contractors are real, but they should not stop your firm from accessing the global talent your projects need. Here comes the role of Remote AE.

Remote AE connects architecture, engineering, and construction firms with pre-vetted virtual assistants, experienced in BIM coordination, CAD production, design documentation, and construction administration, structured for clean, compliant cross-border engagements from day one.

Stop letting tax complexity delay the hiring decision your pipeline is waiting on.

Book a Free Consultation with Remote AE Today, no obligation, no pressure. Just a direct conversation about building your remote AEC team the right way.

FAQs – Tax Implications of Hiring International AEC Contractors

Do I need to issue a 1099 to a foreign contractor?

Generally, no. U.S. forms like 1099-NEC apply to U.S. taxpayers. If the contractor is a non-U.S. person performing services outside the U.S., you typically do not issue a 1099. Keep proper documentation to support their foreign status and where services are performed.

What tax form should an international contractor submit instead of a W-9?

Foreign contractors usually provide a W-8 series form, most commonly W-8BEN (individuals) or W-8BEN-E (entities). These forms certify non-U.S. status and, if applicable, claim treaty benefits. They replace the W-9 used for U.S. taxpayers.

Who pays taxes when you hire an overseas contractor?

In most cases, the contractor pays taxes in their home country. The hiring firm pays the invoice amount. U.S. withholding can apply in specific situations (e.g., U.S.-source income without treaty relief), so confirm the source of income and documentation.

Can hiring a foreign contractor create permanent-establishment risk?

Yes, in some cases. A permanent establishment (PE) risk can arise if the contractor acts like a dependent agent, signs contracts on your behalf, or you maintain a fixed place of business abroad. Keep contractors independent, limit authority, and document the relationship.

Does it matter where the contractor performs the work?

Yes. Location of services affects tax treatment and withholding. Work performed outside the U.S. is generally treated as foreign-source services, while work performed in the U.S. may trigger U.S. tax obligations and reporting requirements.